Gambling with Mother Nature

Gambling with Mother Nature

Climate change brings new risks for homeowners, insurers

By Dale White, dale.white@heraldtribune.com

Dinah Voyles Pulver, dinah.pulver@news-jrnl.com

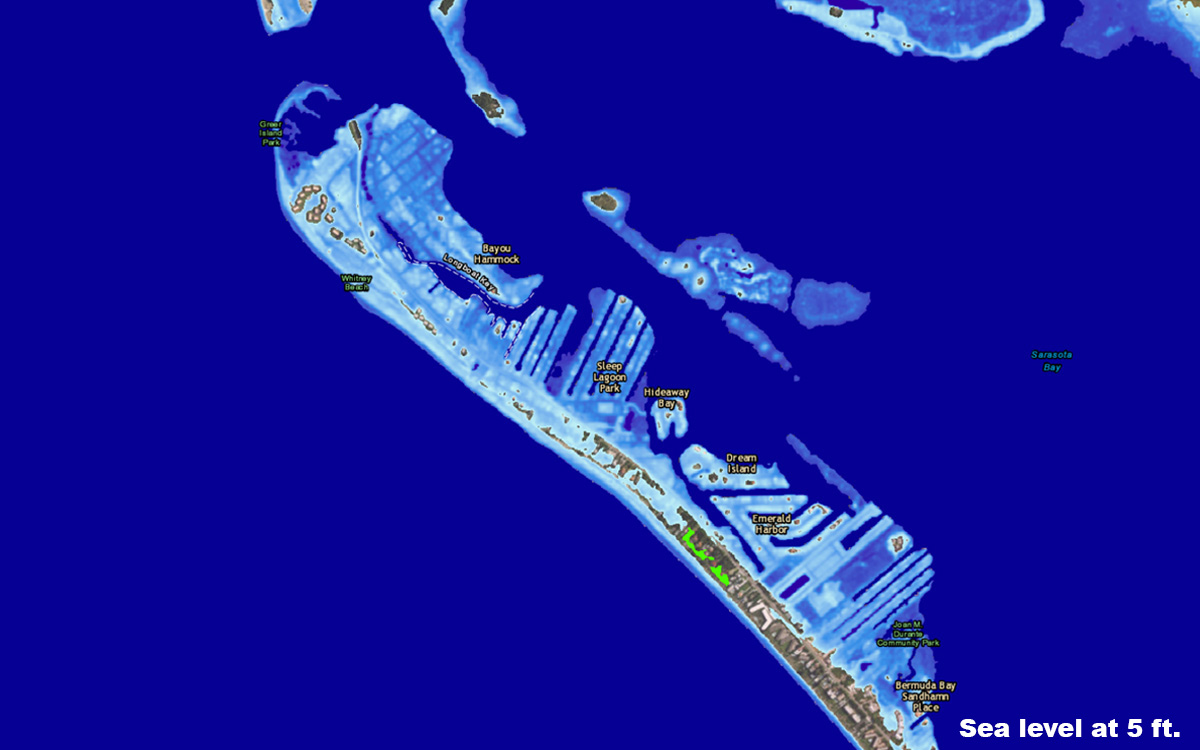

Pete Walker is gambling with his island home near Sarasota Bay — declining to renew his flood insurance and taking his chances with potential storm and water damage.

“It gets in our yard quite often and got in the garage a few times,” Walker said. “One time there was water in the master bedroom.”

Passing cars aggravate the flooding, creating a wake that helps push saltwater onto the Walker property. Yet, when he paid off his mortgage a couple of years ago, Walker declined to renew his flood and hurricane insurance. “That saved me $6,000.”

After 26 years at his Longbeach address, he decided to take the financial risk for any water or storm damage to his wood-frame home, rather than continue to pay premiums that are likely to rise in the years ahead.

“If this place gets wiped out, I’ll sell the property,” Walker vowed.

For Floridians with no debt on their homes by or near the water, dropping the flood or other insurance previously required by their mortgage lenders could become a greater and greater gamble over time — especially if they live in areas affected by rising tides and sea level.

Sunshine State homeowners who must insure their properties are buying policies from an industry that already is reacting to what it sees as global climate change — and its accompanying potential for more frequent flooding and storms and escalating damage claims. That reaction is one of caution that ultimately could call for dramatically increasing premiums — or even declaring some areas too risky to underwrite at any cost.

While politicians still debate whether climate change or the impact — rising sea levels — are real, insurers already are preparing, especially in states like Florida. Besides the cost, the results could impact where people can live.

Before the 2017 hurricane season even began, hail, tornadoes and ice storms elsewhere in the nation in the first quarter the year led to an unprecedented spike in insurance claims of nearly $7 billion. The previous industry average for the same three-month period was $1.5 billion.

“If you were to ask most people if there are more natural disasters, they would say ‘no’” because they do not acknowledge such an event “if it doesn’t hit them,” said Lynne McChristian, Florida representative and catastrophe response director for the Insurance Information Institute.

But the insurance industry knows otherwise, said McChristian, who also is a faculty member at the Florida State University School of Risk Management and Insurance. It is responding to more frequent storms of all types — “not just hurricanes. ... They’re hitting more populated areas. That’s what makes them more costly.”

It could take time for the impacts to dawn on average homeowners.

So far, “sea level rise isn’t a huge concern of people I see,” Jeff Nungesser, owner of Iron City Insurance in Sarasota, said of his clients. “People worry about paying their premiums today. They’ll worry about sea level rise in 30 years.”

For insurance companies, however, sea level rise already is a major consideration.

As an industry based on weighing risk, insurers say denying climate change and its potential consequences, such as sea level rise, is not an option.

“The fact is that climate is changing,” said Don Griffin, vice president of the Property Casualty Insurers Association of America, a trade association that represents more than 1,000 companies that collectively cover 35 percent of the homeowner, business and automobile insurance market. “We’re experiencing a warmer period now.”

Uncertainty of risk

Griffin insists the insurance market is currently well positioned, with the money to handle claims.

“We are strongly capitalized. ... We are in a better principal position than we have been in 50 years,” he said. “We have to have the funds available to pay for losses.”

Over time, the risk is that higher seas and a changing climate will result in more costly disasters. That could change insurers’ attitudes on whether they want to take on those risks.

The concern, McChristian explained, is not a single event such as a tornado — “that is not going to devastate” a company — but what the industry calls a “mega-disaster” causing wide swaths of devastation.

“It is not inconceivable that in any given year there could be more than one mega-disaster,” the Insurance Information Institute warns.

Insurance companies buy “reinsurance” from entities such as Lloyd’s of London. “That reinsurance exists as their financial back-up,” McChristian said. It also enables them to “take on more business.”

“When there isn’t a disaster the money (in the reinsurance market) is plentiful,” McChristian said. After a disaster, however, “investors pull back.”

After a series of disasters, the insurance and reinsurance markets will have to consider “limiting how much they take on in vulnerable areas,” McChristian said.

Policies will not be “canceled,” though that is the term consumers often use, she explained. “Policies are not renewed … People say, ‘I’ve been with them (an insurance company) for 20 years.’ No. You’ve had 20 one-year policies. You have protection for that one year.”

Although a few underwriters may offer homeowners a locked-in rate for a three-year policy, “most do not,” Nungesser said. Just because a property owner’s premium may have held steady for the past year or so, “that’s no guarantee what it will be 12 months from now.”

Even private insurers that offer flood insurance at rates that can be competitive with federally subsidized policies only do so based on “today’s risk,” Nungesser stressed.

Like all insurers, they frequently reassess that risk.

After the eight hurricanes that pummeled Florida in 2004 and 2005, many insurers in Florida stopped renewing policies, upending the market and forcing many property owners into the state-managed Citizens Property Insurance.

If and when that could happen again are lingering possibilities. Paying your yearly premiums is not a long-term guarantee of coverage. Insurance companies are adept at anticipating the possible numbers of house fires and burglaries they may have to cover based on trends, Griffin said, but “Mother Nature is not quite so predictable.”

“People do not appreciate the uncertainty of the risk,” McChristian said. “It’s all about the unknown.”

What is known is that the risk will rise as Floridians continue to build near rising shorelines.

Low to high scenarios

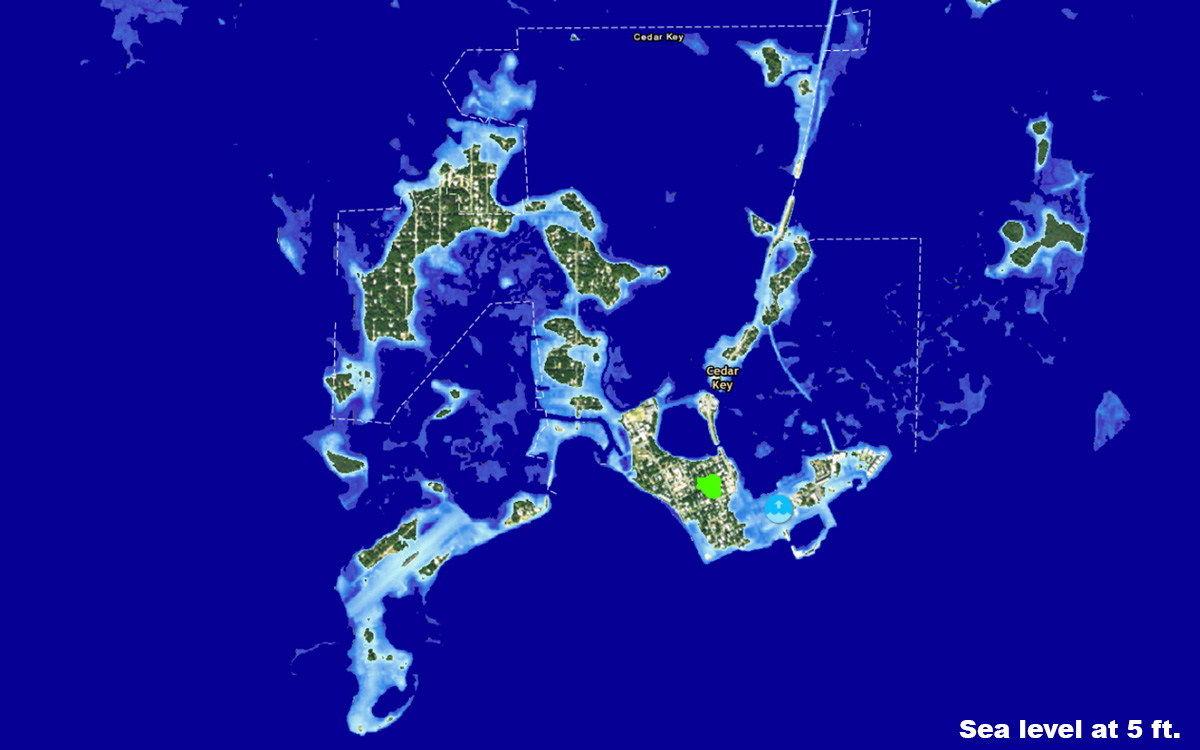

The Union of Concerned Scientists projects that, within the next two decades, nearly 170 coastal communities in the United States will face “chronic” inundation, which it defines as flooding at least 26 times per year or about once every other week.

The organization recently issued projections for the rest of the century for “low,” “intermediate” and “high” scenarios of sea level rise in Florida and which seaside towns are likely to be affected.

The “low scenario” is based on the presumption that carbon emissions will decline steeply and global warming will be limited to less than 2 degrees Celsius. In that case, the scientists foresee nearly 20 Florida communities experiencing sea level rise in some neighborhoods by 2100 — including Longboat Key, the Keys, Merritt Island, Key Biscayne and St. Pete Beach.

The “intermediate scenario” is based on carbon emissions peaking about mid-century and global sea level rise of about four feet with a “moderate” increase in ice melting. That case contributes to extensive sea level rise in the Keys and on Key Biscayne by 2035 and in Miami Beach, St. Pete Beach, Merritt Island and other locales by 2060.

By 2080, the organization states, about 25 more communities would be affected by the “intermediate scenario,” including Longboat Key, Palmetto, Fort Lauderdale and Cocoa Beach.

By 2100, the “intermediate” projections are that nearly 60 Florida communities will, to varying degrees, be coping with rising seas, including Bradenton, Englewood, Miami and the Jacksonville beaches.

The “high scenario” is based on the presumption that greenhouse gas emissions rise through the end of the century causing more ice melt and about 6.5 feet in sea level rise.

If that happens, the organization says that, by 2030, the Keys, Key Biscayne and Cape Sable will be contending with rising sea levels. By 2045, the number of affected Florida communities will grow to nearly 20, including Miami Beach, St. Pete Beach and Melbourne Shores.

By 2060 another 12 could expect to be added to the list, including Longboat Key, Palmetto, Cocoa Beach, Fort Lauderdale, Hollywood, Jacksonville area beaches and Sanibel Island.

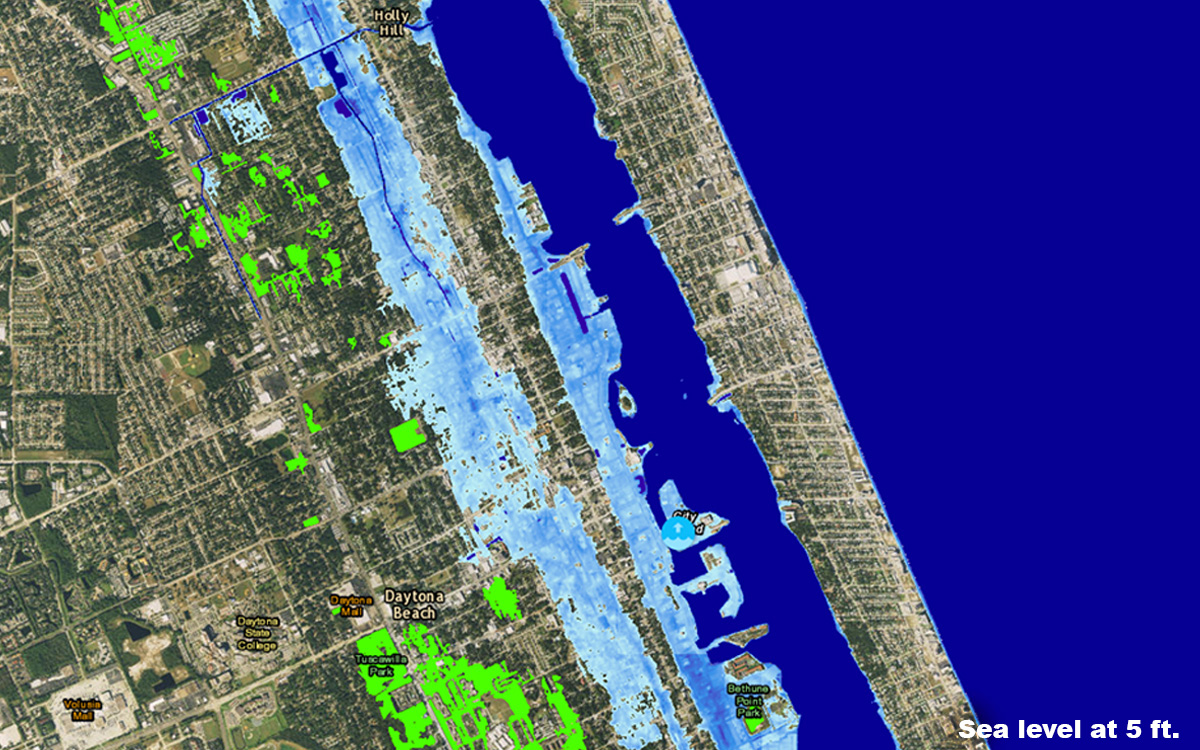

By 2070, the “high scenario” could mean sea water flooding in about 50 communities, including Ormond Beach, Port Charlotte and Englewood.

By the turn of the century, the organization predicts the “high scenario” causing nearly 90 Florida communities to be at least partially submerged.

They would include Venice, Naples, Fort Myers, Apalachicola, Fort Walton Beach, Bradenton, Daytona Beach, Hollywood and Homestead.

Today’s Replacement costs

Bob Lenari, a lifelong resident of Whitaker Bayou in Sarasota, is among Floridians who have decided to no longer insure their homes from storm damage.

He had been paying about $810 annually for flood insurance, with the intention that the $114,000 policy would enable him to rebuild the small home he inherited.

He has since removed the tidal gauge on his dock and declined to renew his federally subsidized insurance for flood damage.

Although Whitaker Bayou is in an area the city of Sarasota regards as being eventually vulnerable to sea level rise attributed to global warming, Lenari sees no cause for immediate concern.

The highest tide he has experienced on the bayou would have to rise another four feet to reach his home, the retired barber said. “I grew up here and I’ve never seen anything close. I’ll insure it myself. If I have to, I’ll tear it down and build another one.”

But replacing a home, especially one that has flooded, can be increasingly expensive, whether for the homeowner or an insurer.

For the insurance industry, several factors come into play in assessing potential damage that were not as evident decades ago, especially in Florida, where 1,000 new residents arrive daily.

“Insurance is tied to building costs,” McChristian said. “It’s all about rebuilding after destruction.”

While a Florida home damaged in a hurricane decades ago may have consisted of a carport and an interior without air conditioning, today’s homebuyer wants more square footage, more lavish furnishings and more expensive amenities.

Adding to that, Griffin stressed, “we have more people on the coasts than we have ever had.”

And they keep coming, buying new structures that conform to the tougher building code Florida adopted after 1992’s Hurricane Andrew, but still putting themselves in potential harm’s way.

Although structures can be constructed for “hurricane resistance,” McChristian said, “there is no hurricane-proof building.”

Inflationary costs of raw construction materials also add to an insurer’s replacement expenses.

According to the Insurance Information Institute: “Hurricane Katrina caused losses of $41.1 billion, the highest on record, about twice as much as Hurricane Andrew would have cost had it occurred in 2005. … If, as suggested, hurricane-related losses grow by as much as 40 percent over the next 20 years, a Katrina-like storm could cause $60 billion in losses, or significantly more if it struck a densely populated metropolitan area like Miami or New York City.”

Increasing risks, decreasing values

Werner Kruck, chief operating officer for Security First Insurance, calls sea level rise the single biggest climate change issue for Florida.

The Ormond Beach-based homeowners insurance provider and underwriter said, “You have inundation slowly but surely, and it creeps in.”

It’s not that the insurance industry is on the hook for all that damage, Kruck said. The federal government writes most flood policies, which would cover the loss for properties that are lost to the sea. But that, said Kruck, has created its own set of potential problems.

The federal flood insurance program, enacted in 1968, relies on taxpayers for its reinsurance or it would otherwise be considered bankrupt. It borrowed nearly $25 billion from the U.S. Treasury to meet its obligations after Hurricanes Katrina, Sandy and Ike, a debt that is not expected to be repaid.

Congress must decide by September whether to renew the troubled program and, if it does, whether to toughen its standards or call for steep hikes in premiums.

The NFIP has about 5 million active policies. It continues to provide coverage for “severe repetitive loss” properties that, according to the Washington Post, have historically accounted for about 30 percent of its claims — allowing homeowners to rebuild, get flooded and rebuild again.

Rising seas are expected to expose more properties in the federal program to flooding and tidal surges. The real estate appraisal firm Zillow estimates that nearly 2 million U.S. homes worth almost $900 billion could be underwater with a six-foot sea level rise by 2100. That estimate equates to nearly 1 million homes in Florida, one in eight, being subject to flooding.

The business of insuring properties at risk from the sea and storm damage is likely to make the economic realities even worse in the years ahead, for the federal government and the private insurance industry, Kruck said.

“Because what happens if I own a home in Miami and all of a sudden the water is starting to lap up on high tide a little bit more, and a little bit more, and a little bit more? The first thing is my home is not worth as much,” Kruck said. “So, what happens is people have high-end real estate and once everybody realizes that it’s only a matter of time before it’s uninhabitable, it becomes worthless.”

“Now, from an insurance point of view, what we do not want to do is insure property at a high replacement value that the owner knows is worthless because you have a higher incentive to cause insurance loss before you have your final flood loss.”

Arson, for example, becomes a huge issue for insurers when people know their properties are going to decrease in value.

“We don’t want as a general rule to insure something for a high limit where the replacement cost significantly exceeds the market value,” he said. “Because then there’s an increasing incentive for that individual to have a loss that’s covered so they don’t have to be exposed to the loss that isn’t covered.”

While Kruck doesn’t necessarily agree with suggestions that insurance companies “need a plan for climate change,” he said the industry is continually getting better at assessing individual risk and pricing premiums accordingly. And that will have impacts as seas rise.

“That’s good for us and it’s good for the majority of insurers,” he said. “It’s bad for the people that we can isolate and say that’s a risk that’s way too high.”

It means the industry will be quicker to avoid writing policies in areas once the industry determines the market value has “dropped next to nothing.”

“Insurance companies will become unwilling to insure properties along the waterfront,” or will “significantly increase the premiums to account for potential losses.”

Finding a company to insure a waterfront property at what the owner believes it is worth will become a problem, he said. Insurance premiums, if a company agrees to write a policy, are likely to become more and more expensive.

“You’ll have an increasing number of businesses and individuals that have a financial loss that’s not covered by anything,” he said. “They’ll probably turn to the government.”

Most homeowners in flood-prone areas already buy their flood insurance from the federal flood insurance program, which writes policies at subsidized rates. And that, said Kruck, has exacerbated the problems that will occur with rising seas.

Federal subsidy conundrum

The federal government “provided subsidized insurance to people so that they would build in low-lying areas that are susceptible to inundation,” Kruck said. Now owners have homes with a mortgage or their life savings wrapped up in at-risk properties.

“And now you say, well, the costs have gone way up on that and who’s going to bear the financial risk for that?”

A few years ago, the federal government tried to enact changes that would allow higher premiums for flood insurance. But protests from people who were facing a tenfold increase in their insurance rates forced the government to scale back those increases.

“At some point in time you would start looking at communities and say it doesn’t make sense to have residences here because the cost of financing or protecting against flooding is so high that you better plow them under and make it a park,” Kruck said. “But that means somebody is going to have a loss.”

If a home is worth $200,000 but the cost of a flood insurance policy is $25,000, a buyer is not going to pay full price for the home, he said.

“The value would have to come down to compensate for the annual cost of flood.”

But, when the federal government subsidizes rates, it encourages people to stay, build and invest in low-lying, flood-prone areas, he said. And if the seas rise an inch, and a hurricane comes in at high tide that’s higher than before, that can mean a lot of damage.

“We put ourselves in a big damn hole is what we have done,” said Kruck. “We’ve got tons of residences in low-lying areas that aren’t paying the economic costs.”

Most private insurers don’t write flood policies. But Kruck said those that do won’t be writing policies if the risk is too high.

In the past, entire communities were given prices for insurance policies based on class. With today’s advanced mapping and technology, companies instantly determine a home’s risk, said Kruck.

“We can assess the flood risk and come up with a price,” he said. “In some areas that price would be a lot higher than the federal price.”

If private insurers begin writing more flood policies in low-risk neighborhoods, that’s likely to leave the federal government on the hook for all the rest.

“It’s all a matter of economics,” Kruck said. “It’s not policy. It’s not politics. It’s economics. Supply and demand. Subsidization."